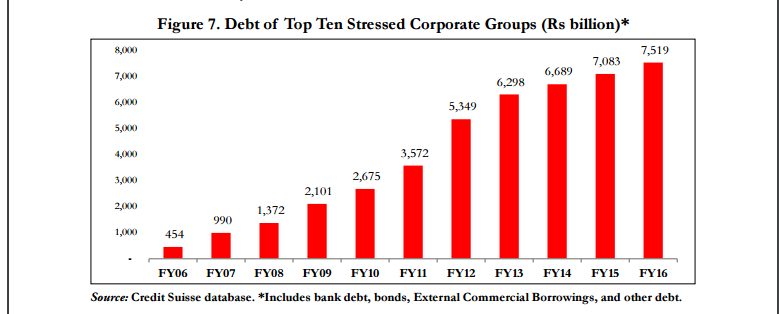

India's twin balance sheet problem is unique mix of over leveraged and distressed companies and one hand and rising NPAs in bank on the other. Twin balance sheet has held up investment and has decelerated India's growth wagon wheel.

Causes of twin balance sheet Problem

the Genesis of twin balance sheet can be found in the early 2000s when the Indian Economy was consistently growing at rate of 8 % the factor leading to rising bank NPA and over leveraged companies are

- Bank lend aggressively when the market and Economy was in Good position.

- Poor regulation and lack of period checks on the profitability and sustainability of the companies and their projects.

- Project bid extremely low tariff with confidence to renew them later but which didn't happened.

- Project delayed due to lack of environmental clearance , growing cost of raw material.

- To resolve the delay in project , bank resorted to ever greening of loans .

Step to be taken

- Loss recognition.

- The AQR was meant to force banks to recognise the true state of their balance sheets. But banks nonetheless continue to evergreen loans, as the substantial estimates of unrecognised stressed assets make clear.

2. Coordination.

- The RBI has encouraged creditors to come together in Joint Lenders Forums, where decisions can be taken by 75 percent of creditors by value and 60 percent by number. But reaching agreement in these Forums has proved difficult, because different banks have different degrees of credit exposure, capital cushions, and incentives. For example, banks with relatively large exposures may be much more reluctant to accept losses. In some cases the firm’s losses aren’t even known, for they depend on the extent of government compensation for its own implementation shortfalls, such as delays in acquiring land or adjusting electricity tariffs. And deciding compensation is a difficult and time-consuming task; many cases are now with the judiciary.

3. Proper incentives.

- The S4A scheme recognises that large debt reductions will be needed to restore viability in many cases. But public sector bankers are reluctant to grant write-downs, because there are no rewards for doing so. To the contrary, there is an inherent threat of punishment, since major write-downs can attract the attention of investigative agencies. Accordingly, bankers have every incentive to simply reschedule loans, in orderto deferthe problems until a later date. To address this problem, the Bank Board Bureau (BBB) has created an Oversight Committee which can vet and certify write-down proposals. But it remains open whether it can change bankers’ incentives.

4. Capital.

- The government has promised under the Indradhanush scheme to infuse Rs 70,000 crores of capital into the public sector banks by 2018-19. But this is far from sufficient, and inherently so, because there is a principal-agent problem, arising from the separation of the institution with financial responsibility (the government) from its decision-making agent (the state banks). If the government promises unduly large funds in advance, the banks may grant excessive debt reductions. But banks do not receive sufficient assurance of funding, they will not be able to grant companies enough debt relief.

Challenges

- difficult to dispose the Assets

- Market over capacity in some sector make more difficult to dispose i.e Steel

- It will be very difficult to recover from service sector and intangible asset

- Govt. and stake holder (bank) may have incur losses due to undervaluation of assets.

0 comments:

Post a Comment